Takaful vs Insurance in UAE: Which One to Choose in 2026

Choosing between Takaful vs insurance in UAE can feel confusing, especially for expats and residents buying health, car, life, or business coverage. Both options protect you from financial loss, but they do not work in the same way. Takaful insurance UAE is based on Islamic principles, while conventional insurance UAE follows a standard risk-transfer model.

This guide explains the difference between Takaful and insurance, when Takaful makes sense, when conventional insurance may be better, and how to choose the right option in 2026.

What is Takaful vs Insurance in the UAE?

Takaful vs insurance in the UAE means comparing Sharia-compliant insurance, based on mutual support, with conventional insurance, based on a contract between the customer and insurer. Takaful is often called Islamic insurance in the UAE because it follows Sharia principles. The UAE Central Bank explains that Takaful companies must comply with Takaful insurance regulations and requirements issued by the Central Bank and the Higher Shari’ah Authority. Conventional insurance is the more common model. You pay a premium to the insurance company, and the insurer agrees to cover approved claims under the policy terms.

The UAE insurance market includes national insurance companies, foreign insurance companies, and Takaful insurance companies, according to the UAE Government portal.

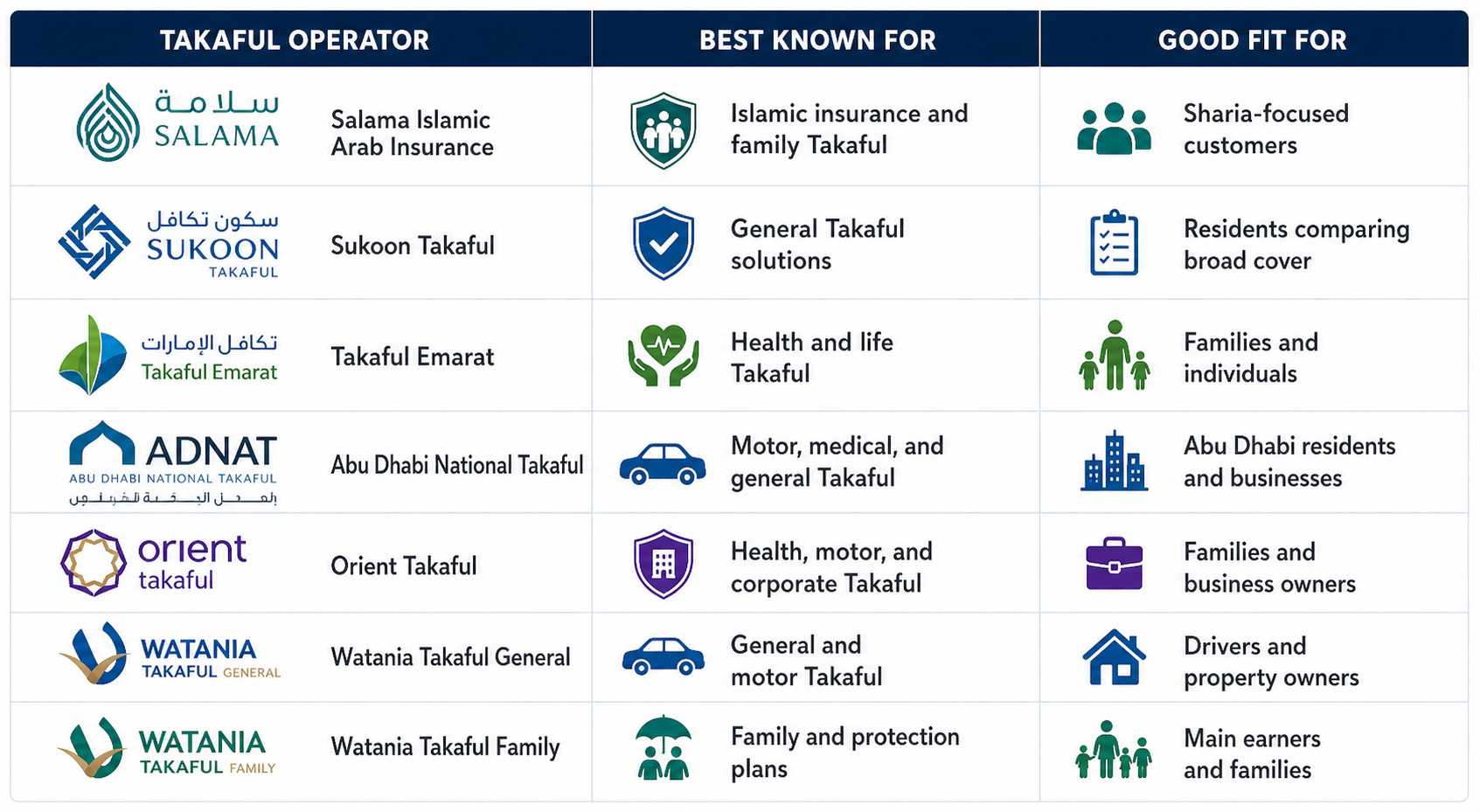

Top Takaful Operators in UAE to Compare in 2026

The UAE has several licensed Takaful insurance operators, so the right choice depends on the policy type, claim support, network access, and whether the plan fits your needs. The Central Bank of the UAE lists licensed Takaful insurance companies, including Salama, Sukoon Takaful, Takaful Emarat, Abu Dhabi National Takaful, Orient Takaful, Watania Takaful, and others.

Takaful Operator | Best Known For | Good Fit For |

Salama Islamic Arab Insurance | Islamic insurance and family Takaful | Sharia-focused customers |

Sukoon Takaful | General Takaful solutions | Residents comparing broad cover |

Takaful Emarat | Health and life Takaful | Families and individuals |

Abu Dhabi National Takaful | Motor, medical, and general Takaful | Abu Dhabi residents and businesses |

Orient Takaful | Health, motor, and corporate Takaful | Families and business owners |

Watania Takaful General | General and motor Takaful | Drivers and property owners |

Watania Takaful Family | Family and protection plans | Main earners and families |

Quick Tip Before Choosing

Do not choose a Takaful operator only because it is Sharia-compliant. Compare the claim process, hospital or garage network, exclusions, renewal cost, customer support, and policy limits before buying.

Takaful Insurance vs Conventional Insurance in the UAE

Point | Takaful Insurance UAE | Conventional Insurance UAE |

Main idea | Mutual support among participants | Risk transfer to insurer |

Religious basis | Sharia-compliant structure | Standard commercial insurance |

Money handling | Participant fund model | Company premium model |

Surplus treatment | May be shared or retained by the fund | Usually belongs to the insurer |

Best for | Sharia-conscious customers | Wider market choice |

Products available | Health, car, family, business | Health, car, life, travel, business |

Main check | Sharia governance and fund rules | Coverage, price, and claims service |

Takaful and conventional insurance can both cover similar risks. The real difference is in the structure, money handling, and governance. If your main concern is Sharia-compliant insurance UAE, Takaful is the better starting point. If your main concern is wider provider choice, faster comparison, or very specific add-ons, conventional insurance may give more options.

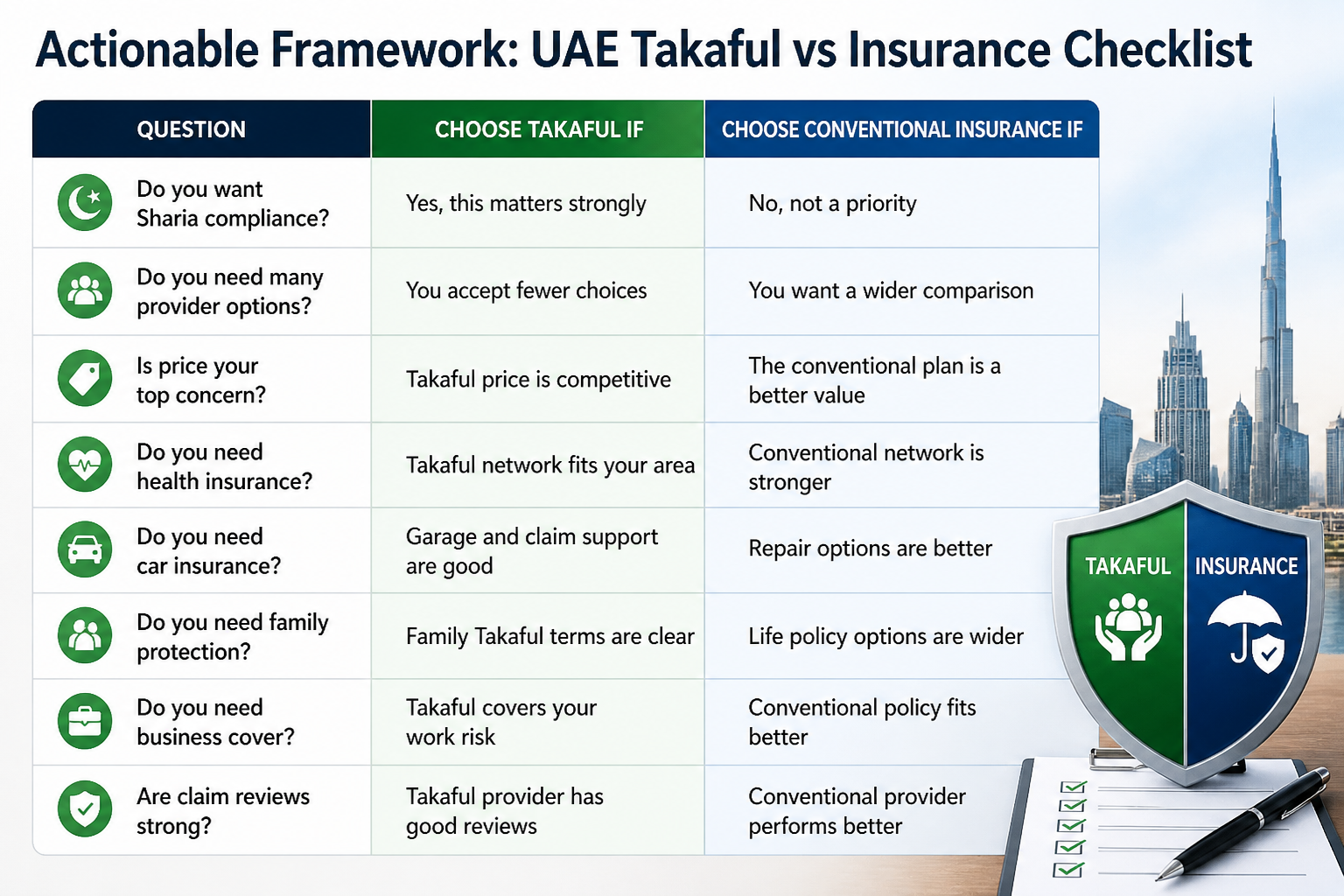

How to Get Started: Diagnose the Right Fit

Decide what you need covered

Start with health, car, travel, home, life, or business insurance.Check if Sharia compliance matters

If it matters to you, shortlist licensed Takaful providers first.Compare coverage limits carefully

Look at claim limits, exclusions, deductibles, and co-payments.Review the provider list

The UAE Central Bank lists licensed Takaful companies, including Salama, Sukoon Takaful, Takaful Emarat, Abu Dhabi National Takaful, Orient Takaful, and Watania Takaful.Check claim process details

Ask how claims are filed, approved, rejected, and escalated.Compare customer support quality

Choose a provider that answers clearly before you pay.Review total cost, not just premium

Include deductibles, co-payments, add-ons, and renewal changes.

Foundational Strategy

Start with your actual need, not the product name. If you want Islamic insurance UAE, compare licensed Takaful providers and check the policy terms. If Sharia compliance is not your main concern, compare both Takaful and conventional insurance side by side.

Tools Strategy

Use comparison sites, provider websites, UAE insurance reviews, policy PDFs, and customer support chats to compare details. Focus on coverage limits, exclusions, network access, claim steps, renewal price, and complaint history. These details matter more than a small premium difference.

Professional Strategy

Speak to a licensed broker or advisor if your case is complex. This is useful for families, business owners, high-value vehicles, medical needs, or life protection. Ask the advisor to explain both Takaful vs conventional insurance UAE options in simple terms.

Use this checklist before buying or renewing. The right answer may vary depending on your emirate, family size, car value, and medical needs.

How Takaful Can Vary by Emirate

Takaful may vary by emirate in terms of network access, health insurance rules, pricing, and claim handling. But the core Takaful structure remains the same across the UAE because licensed Takaful operators adhere to UAE-level regulations and Sharia governance.

Conclusion and Next Steps

Choosing between Takaful vs insurance in UAE should be practical, not emotional. Before buying, check:

Your need for Sharia compliance

Coverage limits and exclusions

Hospital or garage network quality

Claim process and support speed

Total cost after deductibles

Provider licensing and reputation

Your next step is simple: compare one Takaful option and one conventional insurance option for the same coverage type. Then choose the policy that gives better protection, clearer terms, and stronger claim support.

Frequently Asked Questions

What is the difference between Takaful and insurance?

Takaful is a Sharia-compliant insurance model based on mutual support among participants. Conventional insurance is a standard insurance contract where the insurer accepts risk in return for a premium.

Is Takaful better than insurance in the UAE?

Takaful is better if you want Sharia-compliant insurance UAE and the policy gives the coverage you need. Conventional insurance may be better if it offers stronger network access, better pricing, or more suitable add-ons.

How does Takaful work in UAE?

Takaful works through a participant fund where members contribute to support covered claims. The provider manages the fund under Takaful rules and Sharia governance.

Is Takaful more expensive than conventional insurance?

Not always. Takaful vs insurance cost UAE depends on the provider, policy type, claim history, coverage limits, and add-ons. Always compare the total cost, not only the premium.

Related Posts

Best Insurance Company in UAE 2026: Choose Right

Learn how to choose the best insurance company in the UAE 2026 by comparing coverage, claims, reviews, support, networks, and policy terms.

Insurance Claim Rejection In UAE: Reasons & Fixes

Insurance claim rejection in UAE can happen due to missing proof, exclusions, delays, or wrong filing. Learn the real reasons and fixes for 2026.