Hidden UAE Health Insurance Gaps Expats Miss

A health insurance card can feel like protection until the hospital asks for approval, a co-pay, or full payment up front. For many expats in the UAE, the surprise does not come when they buy the policy. It comes when they actually need to use it. The plan may be valid, the premium may be paid, and the insurer may be approved, yet the real experience can still be frustrating if the policy has limits that were not clear at the start.

UAE health insurance is mandatory for many residents, but “mandatory” does not always mean “complete.” Dubai requires employers to provide health insurance for employees, while sponsors are responsible for dependents. Abu Dhabi has stronger dependent coverage rules for employers, including one spouse and up to three children under 18 in many employment cases. From 2025, employer health insurance requirements also expanded more broadly across the UAE for private-sector employees and domestic workers.

That is where many expats get caught. They assume the card is enough. The hidden side is in the fine print.

Why UAE Health Insurance Feels Clear Until You Use It

Most expats look at three things when comparing health insurance in the UAE: premium price, hospital network, and whether the plan is “basic” or “comprehensive.” That is a start, but it misses the parts that affect real bills. A cheaper plan can look fine if you only need a quick GP visit. It can become expensive when you need scans, specialist care, surgery, maternity treatment, or long-term medication.

Online expat discussions often show the same pattern. People ask why a pre-existing condition is not fully covered, why premiums increase sharply for older family members, or why a treatment needs approval even when the hospital is in-network. Recent Reddit discussions about UAE health insurance highlight recurring concerns about pre-existing conditions, high premiums, co-pays, and what to check before buying.

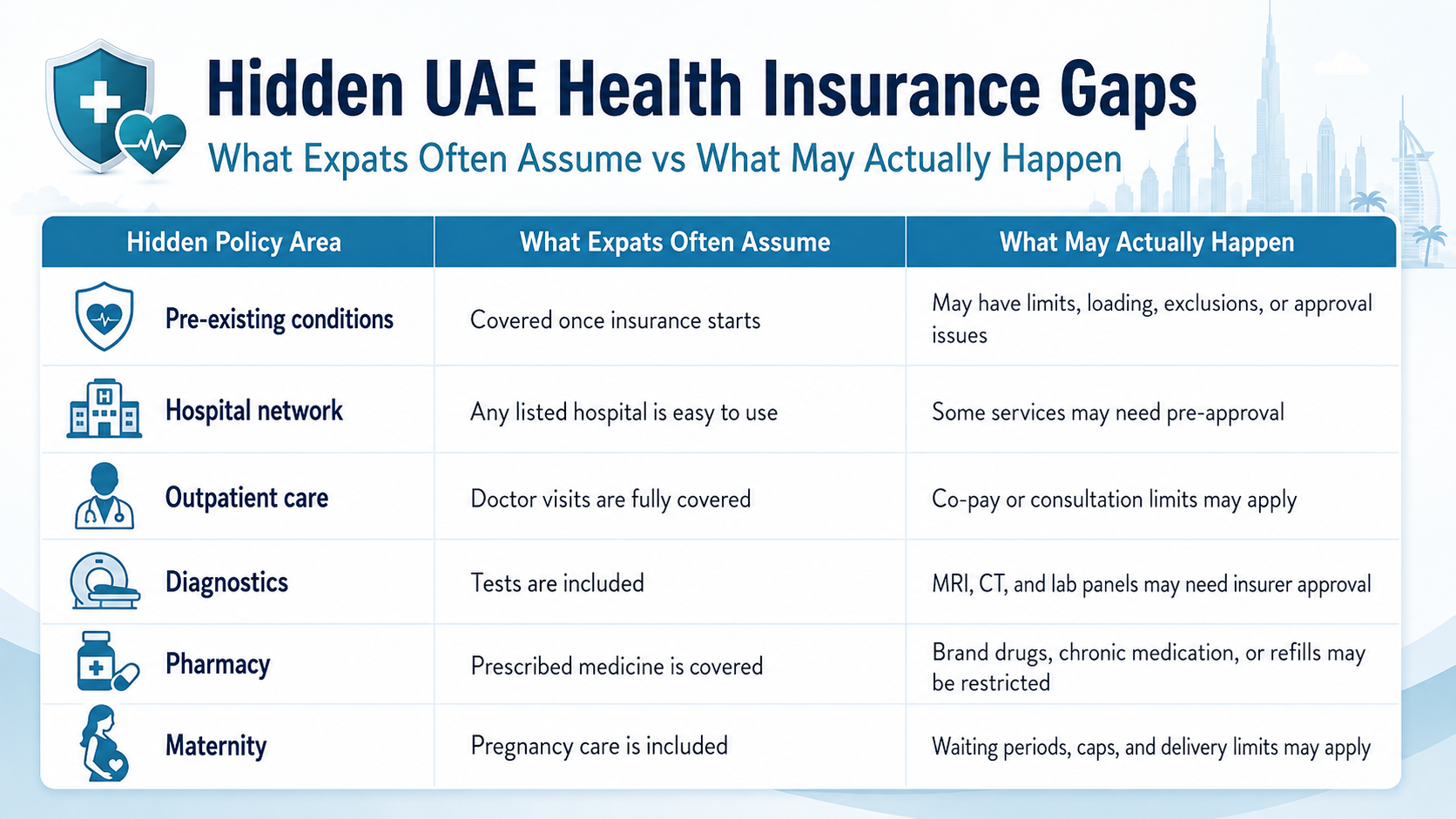

The Fine Print Expats Often Miss

Here is where the hidden cost usually sits.

Hidden Policy Area | What Expats Often Assume | What May Actually Happen |

Pre-existing conditions | Covered once insurance starts | May have limits, loading, exclusions, or approval issues |

Hospital network | Any listed hospital is easy to use | Some services may need pre-approval |

Outpatient care | Doctor visits are fully covered | Co-pay or consultation limits may apply |

Diagnostics | Tests are included | MRI, CT, and lab panels may need insurer approval |

Pharmacy | Prescribed medicine is covered | Brand drugs, chronic medication, or refills may be restricted |

Maternity | Pregnancy care is included | Waiting periods, caps, and delivery limits may apply |

The biggest mistake is reading the benefit list but not the conditions attached to each benefit.

Pre-Existing Conditions Can Change Everything

This is one of the most painful areas for expats. A pre-existing condition is usually any health issue, symptom, diagnosis, surgery, or ongoing treatment that existed before the policy started. It may include diabetes, hypertension, thyroid issues, asthma, cancer history, heart problems, back issues, or even earlier test findings. Some plans may cover pre-existing conditions after declaration. Some may cover them with limits. Others may increase the premium or exclude related treatment. In expat forum discussions, pre-existing conditions are one of the most common reasons people feel shocked by UAE health insurance quotes or claim decisions.

The mistake is not declaring the condition. That can create bigger problems later because insurers may review medical history when a claim is submitted.

Co-Pay Looks Small Until Treatment Repeats

A 10 percent or 20 percent co-pay may sound harmless. On a single consultation, it may be. On repeated specialist visits, diagnostic tests, physiotherapy, or long-term prescriptions, it adds up. For example, an expat managing diabetes may pay co-payments for:

Endocrinologist visits

Lab tests

Regular medication

Follow-up appointments

The policy may technically cover care, but the resident still pays a noticeable share each month. This is why UAE medical insurance should not be judged only by the annual premium. A low premium with high co-pay can cost more across the year than a better plan with a higher upfront price.

Network Access Is Not Always Simple

A hospital or clinic logo on the insurer’s network list does not always mean every doctor, department, treatment, or test is fully accessible. Some facilities may be covered only under certain plan tiers. Some specialists may require referral. Some treatments may need pre-authorization. Emergency care may be treated differently from planned care. This is where expats often feel misled, even when the insurer has followed the policy wording. The gap is usually between “network available” and “treatment approved.”

Before booking treatment, it is better to ask: “Is this doctor, procedure, test, and department covered under my exact policy number?” That one question can prevent a bad billing surprise.

Maternity Cover Has More Conditions Than Many Expect

Maternity insurance in the UAE can be confusing because pregnancy-related care is not always treated like normal outpatient care. Many plans have:

Waiting periods before maternity benefits apply

Caps on normal delivery and C-section costs

Separate limits for prenatal consultations

Exclusions for pregnancy are already confirmed before the policy starts

Expats planning a family should not wait until pregnancy to check coverage. By then, switching or upgrading may not solve the issue.

Dependents May Not Be Covered the Way Employees Are

This is another area where UAE expats discover differences too late. An employee may have employer-provided health insurance, but a spouse, child, parent, or domestic worker may need separate coverage depending on the emirate, sponsor type, and employer policy.

Dubai and Abu Dhabi do not work exactly the same way. Dubai places responsibility for dependents on the sponsor, while Abu Dhabi rules include employer obligations for certain family members. UAE government guidance confirms that employer and sponsor duties differ by emirate. For families, this matters because dependent plans can be more expensive than expected, especially for older parents or anyone with a medical history.

Renewal Can Bring a Different Problem

A plan that worked last year may not remain affordable this year. Premiums can change due to age, claims history, medical inflation, policy changes, or insurer pricing. Expats often notice this when covering parents, spouses with chronic conditions, or children needing regular care. The hidden side here is dependency. Once someone is on ongoing treatment, switching insurers may become harder or more expensive because the new insurer may review the medical history.

How Expats Can Avoid Late Surprises

Before buying or renewing UAE health insurance, ask for the policy wording, not just the brochure. Then check these items carefully:

Exact hospital and clinic network

Co-pay for outpatient, pharmacy, and diagnostics

Pre-existing condition rules

Annual limit and sub-limits

Maternity waiting period and delivery cap

Dental, optical, and mental health coverage

Emergency treatment rules

Claim reimbursement process

Exclusions list

Renewal terms and age-related pricing

Do not rely only on what a salesperson says in a call. Ask for written confirmation, especially for pre-existing conditions, maternity, chronic medication, and preferred hospitals.

Conclusion: The Real Cost Is Usually in the Details

The hidden side of UAE health insurance is not that policies are useless. The real issue is that many expats buy coverage without understanding how the plan behaves during real treatment. A policy can meet residency requirements and still leave gaps. It can include a hospital network, but still requires approval. It can cover outpatient care but still charge a co-pay. It can mention maternity, but still apply waiting periods and limits.

Frequently Asked Questions

What is the biggest health insurance mistake expats make in the UAE?

The biggest mistake is choosing the cheapest policy without checking exclusions, co-pay, hospital network limits, and pre-existing condition rules. The premium is only one part of the real cost.

Does UAE health insurance cover pre-existing conditions?

Some plans may cover pre-existing conditions, but terms vary. Coverage may include waiting periods, higher premiums, exclusions, or claim approval requirements. Always declare medical history honestly.

Are dependents automatically covered under UAE health insurance?

Not always. Employee coverage and dependent coverage depend on emirate rules, sponsor responsibility, and employer policy. Dubai and Abu Dhabi have different requirements.

Can UAE health insurance premiums increase at renewal?

Yes. Premiums may increase due to age, claim history, insurer pricing, medical inflation, or changes in benefits. Older dependents and people with chronic conditions often face higher renewal costs.

Related Posts

Best Insurance Company in UAE 2026: Choose Right

Learn how to choose the best insurance company in the UAE 2026 by comparing coverage, claims, reviews, support, networks, and policy terms.

Insurance Claim Rejection In UAE: Reasons & Fixes

Insurance claim rejection in UAE can happen due to missing proof, exclusions, delays, or wrong filing. Learn the real reasons and fixes for 2026.