Can UAE Insurance Increase After One Claim?

You make one claim. The car gets repaired. The issue feels closed. Then renewal time comes, and your insurance quote is higher than expected. This is a common concern for UAE residents, especially with car insurance. Some drivers see only a small change. Others lose their no-claims discount or receive a renewal price that feels much higher than the repair claim itself. So, can UAE insurance increase after one claim?

Yes, it can. But it is not automatic in the same way for everyone. The increase depends on the claim type, fault status, repair cost, insurer rules, no-claims history, and the wider insurance market.

Why One Claim Can Affect Your Insurance Renewal

Insurance companies look at claims history before renewal. If you made a claim during the policy year, the insurer may see your profile as slightly higher risk than before. This is especially true if:

You were at fault

The repair cost was high

The claim involved agency repair

The car was expensive to fix

You already had past claims

You lost your no-claims discount

Gargash Insurance explains that claims history can affect UAE car insurance renewal terms, with claim frequency, claim severity, risk assessment, and no-claims bonus all playing a role. That means the renewal increase is not only about one accident. It is about how the insurer reads that claim.

What Residents Usually Notice After One Claim

For many UAE drivers, the biggest surprise is not the claim approval. It is the renewal quote. Some residents report that after one small at-fault accident, their premiums increased sharply. Others say their quote stayed the same because the claim was minor, not their fault, or because they had a long, clean record.

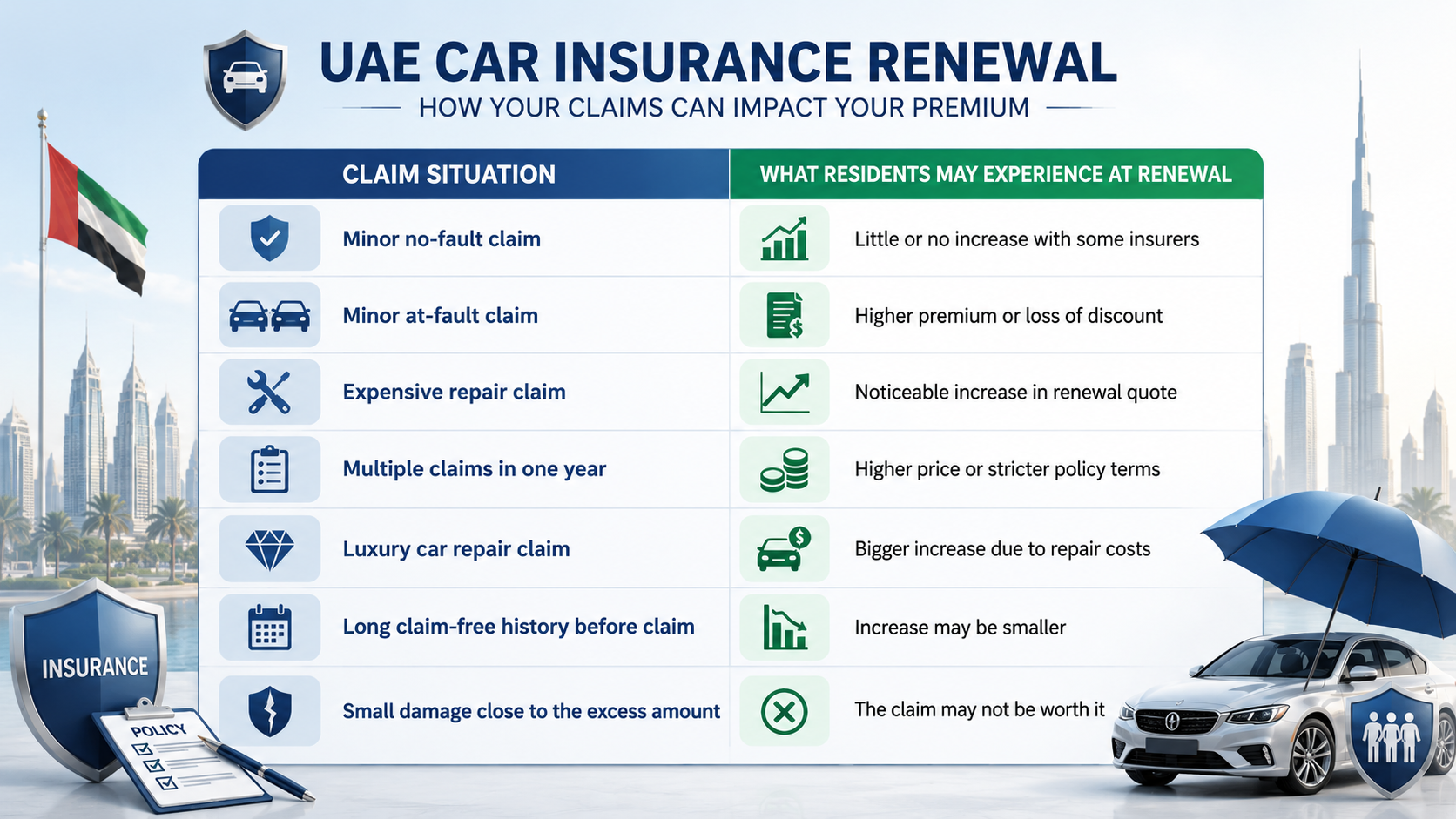

Here is the simplest way to understand what may happen:

Claim Situation | What Residents May Experience at Renewal |

Minor no-fault claim | Little or no increase with some insurers |

Minor at-fault claim | Higher premium or loss of discount |

Expensive repair claim | Noticeable increase in renewal quote |

Multiple claims in one year | Higher price or stricter policy terms |

Luxury car repair claim | Bigger increase due to repair costs |

Long claim-free history before claim | Increase may be smaller |

Small damage close to the excess amount | The claim may not be worth it |

This is the table most UAE residents should focus on before deciding whether to claim or pay directly.

The No-Claims Discount Problem

A no-claims discount rewards you for not making claims during your policy period. If you stay claim-free, your insurer may offer a lower renewal price. If you make a claim, especially an at-fault claim, that discount may be reduced or removed.

This is where many residents feel the price jump. Your premium may rise because of two things happening together:

The insurer adds risk loading after the claim

Your no-claims discount becomes lower

GIG Gulf notes that a no-claims discount does not stay fixed forever and that a claim can reduce or reset it. It also explains that market conditions can still raise premiums even when a customer has a discount. So, if your renewal price increases after a claim, it may not be only because of the repair bill. It may also be because you lost the discount you had built over time.

At-Fault Claims Usually Hurt More

Fault status matters a lot. If the claim was not your fault, some insurers may treat it more lightly. If the claim was your fault, the premium impact is usually stronger. This is why the police report and accident documents matter. They help show whether you were responsible for the accident or whether another party caused it.

A UAE car insurance guide from Shory explains that at-fault claims can affect the no-claims discount, while no-fault claims may not affect it the same way.

Repair Cost Can Matter More Than the Accident Size

A small-looking accident can still become an expensive insurance claim. Modern cars have sensors, cameras, imported parts, radar systems, and costly paintwork. Even a minor front bumper hit can become expensive if the car has advanced driver assistance features. Claims can cost more when they include:

Agency repair

Luxury vehicle parts

Airbag or sensor damage

Windscreen camera calibration

Imported spare parts

Paint and bodywork

Towing and recovery

Replacement car benefits

This is why a claim on a premium SUV can affect renewal more than multiple claims on a basic sedan.

Should You Claim for Small Damage?

Not every small repair needs an insurance claim. If the damage is cosmetic and the repair cost is close to your policy's excess, it may be smarter to pay the repair cost directly. Your excess is the amount you must pay before the insurer covers the rest. For example, if a small scratch costs AED 600 to fix and your excess is AED 500, the actual insurance benefit may be too small. You could save only AED 100 now, but risk losing a better renewal price later.

New India Assurance UAE advises drivers to avoid unnecessary claims and highlights that a claim-free history can help with no-claims discounts at renewal. A claim makes more sense when the repair cost is clearly higher than your excess, the damage affects safety, or the vehicle needs proper documented repair.

Can Health Insurance Increase After One Claim in the UAE?

Health insurance works differently from car insurance. One medical claim may not always lead to a direct personal premium increase, especially if you are covered under an employer group plan. In group health insurance, the insurer usually looks at the company's overall claims experience, not just one employee's. For individual health insurance, renewal pricing can be affected by:

Age

Medical inflation

Plan benefits

Chronic conditions

Claim history

Network type

Insurer rules

So yes, health insurance can become more expensive after claim-heavy usage, but it is not always as simple as “one claim equals a higher premium.”

Can Home or Property Insurance Increase After One Claim?

Yes, property insurance can also increase after a claim. This is more likely when the claim was expensive, repeated, or linked to a risk that may happen again. Examples include:

Water leakage

Fire damage

Theft

Storm or flood damage

Business stock damage

Equipment breakdown

Repeated maintenance issues

For business insurance, one large claim may lead to higher premiums, higher deductibles, exclusions, or stricter inspection requirements before renewal.

Why Your Renewal Can Rise Even Without a Claim

This part confuses many residents. Sometimes your insurance renewal increases even if your own claim was small. Sometimes it increases even when you did not claim at all. That can happen because of:

Higher repair costs across the UAE

More expensive spare parts

Medical cost inflation

Flood or weather-related claim pressure

Insurer-wide price adjustments

Vehicle value changes

Changed underwriting rules

Add-ons included in renewal

Khaleej Times reported that UAE motorists involved in accidents and filing claims may face higher auto insurance premiums, while wider motor insurance premiums have also seen movement in the market.

So, your claim matters, but it is not the only factor behind renewal pricing.

What to Do If Your Insurance Increases After One Claim

Do not accept the first renewal quote without checking your options. Try these steps:

Ask your insurer why the premium increased

Confirm whether your no-claims discount was removed

Share proof if the claim was not your fault

Compare quotes from other insurers

Check broker and insurer portals

Ask for a higher voluntary excess if suitable

Remove add-ons you do not need

Consider garage repair instead of agency repair

Ask for a no-claims certificate if eligible

Start renewal comparison before the expiry date

Shopping around matters. One insurer may increase your renewal sharply after a claim, while another may still offer a better price.

Conclusion

UAE insurance can increase after one claim, especially when the claim is at fault, expensive, or linked to a lost no-claims discount. For car insurance, the impact is usually more direct. For health insurance and property insurance, renewal pricing depends on wider factors such as usage, risk, medical costs, property condition, and insurer rules.

The best decision is not always to claim or not claim. The best decision is to compare the repair cost, policy excess, fault status, and possible renewal impact before filing a small claim.

Frequently Asked Questions

Can UAE car insurance increase after one claim?

Yes, UAE car insurance can increase after one claim, especially if the claim was at fault or expensive. The increase depends on your insurer, car type, claim history, and no-claims discount.

Will my insurance increase if the accident was not my fault?

It may not increase, or the increase may be smaller. Keep the police report and claim documents to prove that you were not responsible for the accident.

Does one claim remove my no-claims discount in the UAE?

An at-fault claim can reduce or remove your no-claims discount, depending on your insurer and policy terms. A no-fault claim may be treated differently.

Can I change insurers after making a claim?

Yes, you can compare and switch insurers at renewal. Your claim history may still be checked, but another insurer may offer a better price.

Related Posts

Best Insurance Company in UAE 2026: Choose Right

Learn how to choose the best insurance company in the UAE 2026 by comparing coverage, claims, reviews, support, networks, and policy terms.

Insurance Claim Rejection In UAE: Reasons & Fixes

Insurance claim rejection in UAE can happen due to missing proof, exclusions, delays, or wrong filing. Learn the real reasons and fixes for 2026.