Insurance Claim Rejection In UAE: Reasons & Fixes

Insurance claim rejection in the UAE is frustrating because most people only read the policy properly after something goes wrong. For expats and residents, a rejected claim can mean paying for hospital bills, car repairs, travel losses, or business damage from your own pocket. The hard part is that many rejections are not random. They usually happen due to missing documents, policy exclusions, late reporting, incorrect claim steps, or unclear communication.

This guide explains why claims are rejected in UAE insurance, how to fix common issues, and how to file an insurance claim in the UAE, with support from residents who can provide the right proof.

What is Insurance Claim Rejection in the UAE?

Insurance claim rejection in the UAE means an insurer refuses to pay a claim, fully or partly, because the claim does not meet the policy terms, lacks supporting documentation, falls under an exclusion, or was not filed correctly. A rejection is not always final. In many cases, you can ask the insurer for the exact written reason, submit missing documents, request a review, or raise a complaint with the right authority. For insurance company complaints, UAE consumers can use Sanadak, which handles complaints against insurance companies licensed by the Central Bank of the UAE. The platform says complaints are free for consumers and SMEs, while appeals cost AED 500.

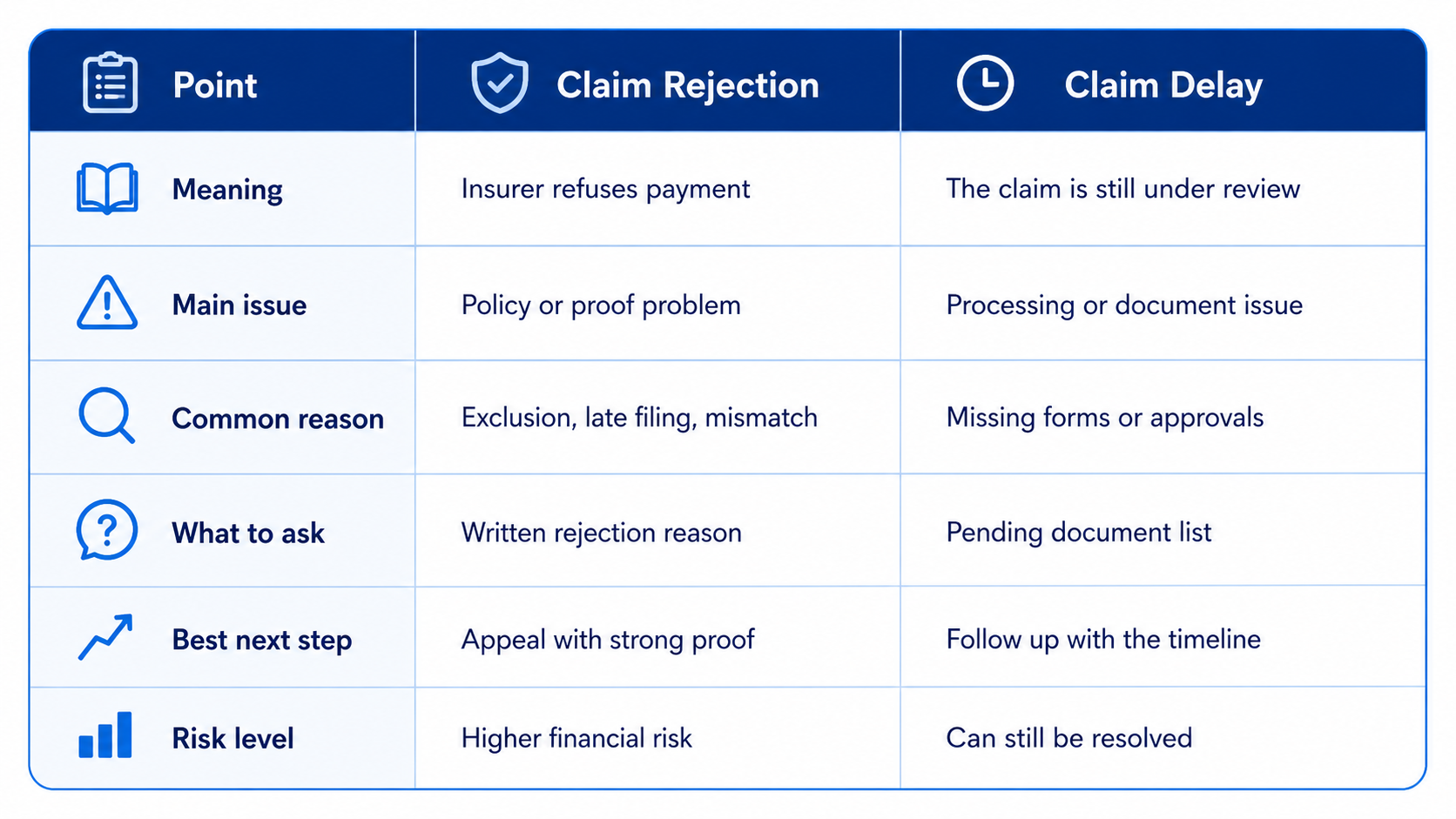

Claim Rejection vs Claim Delay

Point | Claim Rejection | Claim Delay |

Meaning | Insurer refuses payment | The claim is still under review |

Main issue | Policy or proof problem | Processing or document issue |

Common reason | Exclusion, late filing, mismatch | Missing forms or approvals |

What to ask | Written rejection reason | Pending document list |

Best next step | Appeal with strong proof | Follow up with the timeline |

Risk level | Higher financial risk | Can still be resolved |

Use this comparison to quickly understand whether your UAE insurance claim is fully rejected or simply delayed, so you can take the right next step.

Top Reasons Insurance Claims Get Rejected in the UAE

Most rejected claims fall into a few clear patterns. These apply across health insurance, car insurance, travel insurance, home insurance, and business insurance.

1. Missing or incomplete documents

Insurers need proof before they pay. If you submit weak or incomplete documents, the claim may be delayed or rejected. Common missing documents include:

Police report for accident claims

Medical report for treatment claims

Original invoices and receipts

Policy copy and Emirates ID

Claim form with correct details

Photos showing loss or damage

2. The claim falls under exclusions

Every policy has exclusions. These are situations the insurer does not cover. For example, a health policy may exclude certain treatments, waiting-period cases, or non-approved providers. A car policy may not cover damage caused by misuse, racing, or driving outside the agreed policy terms.

3. Late claim reporting

Many policies have reporting deadlines. If you wait too long, the insurer may argue that the delay affected verification. This is common in motor insurance claims, where accident details, police reports, and repair approvals matter. The UAE Central Bank’s motor insurance material explains that third parties or injured parties can submit claims for compensation arising from the insured vehicle, but the claim still requires proper documentation and a proper process.

4. Treatment was not pre-approved

For health insurance, some treatments need pre-approval before the hospital or clinic proceeds. If approval is skipped, the insurer may reject the claim later. This often happens with specialist procedures, scans, surgeries, maternity services, dental treatment, and planned admissions.

5. Wrong provider or garage used

Health insurance plans usually have a network of approved hospitals, clinics, and pharmacies. Car insurance plans may have approved garages or agency repair rules. If you use a provider outside your network without emergency approval, the insurer may reduce or reject the claim.

6. Policy had expired or was not active

If the incident happened before the policy started or after it expired, the insurer usually has a clear reason to reject the claim. This is one of the simplest claim problems to avoid. Keep renewal dates saved in your phone and email.

7. Wrong or unclear information

Claims can get rejected when the information does not match. This includes names, dates, accident details, diagnosis codes, invoice amounts, or vehicle information. Even small errors can slow down approval.

How to File an Insurance Claim in the UAE: Step-by-Step

Report the incident immediately

Inform the insurer as soon as possible. Do not wait until documents become difficult to collect.Collect the right proof first

Get police reports, medical reports, invoices, receipts, photos, approvals, and claim forms.Check your policy terms

Review exclusions, claim limits, network rules, deductibles, and approval requirements.Submit through the correct channel

Use the insurer’s app, website, email, broker, TPA, hospital desk, or claims portal.Ask for a claim reference number

This helps you track the claim and prove submission.Follow up in writing

Use email or official support channels, not only phone calls or WhatsApp messages.Request written rejection details

If rejected, ask for the exact reason, policy clause, and missing documents.

Where to Escalate a Rejected Insurance Claim in the UAE

If your insurance claim is rejected, delayed, or left unresolved, do not stop at the first response. Ask the insurer for a written explanation, the exact policy clause, and the list of missing documents. If the issue still remains unresolved, you can escalate it to the appropriate UAE authority.

Solutions and Strategies

Foundational fixes

Start with the basics. Most claim problems can be reduced before they happen.

Read exclusions before buying the policy

Save all policy documents clearly

Use approved hospitals and garages

Report incidents as soon as possible

Keep invoices, reports, and photos

Ask for pre-approval when needed

Conclusion and Next Steps

Insurance claim rejection in UAE cases is often fixable when you know the real reason. Here is the practical recap:

Ask for rejection reasons in writing

Match the reason with policy terms

Collect proof before filing claims

Use approved providers and garages

Request pre-approval when required

Escalate through official complaint channels

Your next step is simple: create a folder for every policy you own, save your insurance cards, renewal dates, claim contacts, exclusions, and complaint channels. When something happens, you will not be starting from zero.

A rejected claim is not always the end. With the right documents, written proof, and a clear escalation path, many UAE insurance claim problems can be reviewed, corrected, or formally challenged.

Frequently Asked Question

Why does an insurance claim get rejected in the UAE?

Claims are usually rejected because of exclusions, missing documents, late reporting, expired policies, improper provider use, or lack of pre-approval. The fastest fix is to ask for the rejection reason in writing and compare it with your policy terms.

How do I file an insurance claim in the UAE?

Start by reporting the incident to your insurer, then collect the required documents and submit the claim through the insurer’s approved channel. Keep the claim reference number and follow up in writing.

Can I challenge an insurance claim rejection in the UAE?

Yes, you can challenge a rejection by asking the insurer for a written reason and submitting extra proof. If the issue remains unresolved, you can use the correct complaint channel, such as Sanadak, DHA, or DoH, depending on the claim type and emirate.

What should I do first after a claim rejection?

Ask for a written rejection reason, the policy clause used, and the missing document list if any. Then prepare a clean appeal with proof, timeline, invoices, and all communication records.

Related Posts

Best Insurance Company in UAE 2026: Choose Right

Learn how to choose the best insurance company in the UAE 2026 by comparing coverage, claims, reviews, support, networks, and policy terms.

Takaful vs Insurance in UAE: Which One to Choose in 2026

Compare Takaful vs insurance in UAE for 2026. Learn the key differences, costs, benefits, and which option fits your health, car, family, or business needs.