Choosing the best insurance company in the UAE 2026 is not about finding the cheapest premium on a comparison site. For expats and UAE residents, the right insurance provider should be easy to deal with before, during, and after a claim. A low price is useful, but it means little if the hospital network is weak, the repair process is slow, or customer support disappears when you need help.

This guide explains how to choose insurance that UAE residents can trust, what to check in UAE insurance reviews, and how to compare providers without getting stuck in sales talk.

Choosing the right insurance provider in the UAE means selecting a licensed insurer, broker, or policy channel that offers suitable coverage, clear terms, reliable claims handling, fair pricing, and support that matches your health, car, family, travel, or business needs. The UAE government states that the Central Bank of the UAE registers and licenses insurance companies to practice insurance activity in the country. This makes licensing one of the first checks before you compare price, reviews, or benefits. A good provider should make the policy easy to understand. You should know what is covered, what is excluded, how to claim, who to call, and what you may pay from your own pocket.

The UAE has many licensed insurance companies, so the “best” provider depends on your policy type, budget, claim needs, and location. The Central Bank of the UAE registers and licenses insurance companies in the country, so always check licensing before buying.

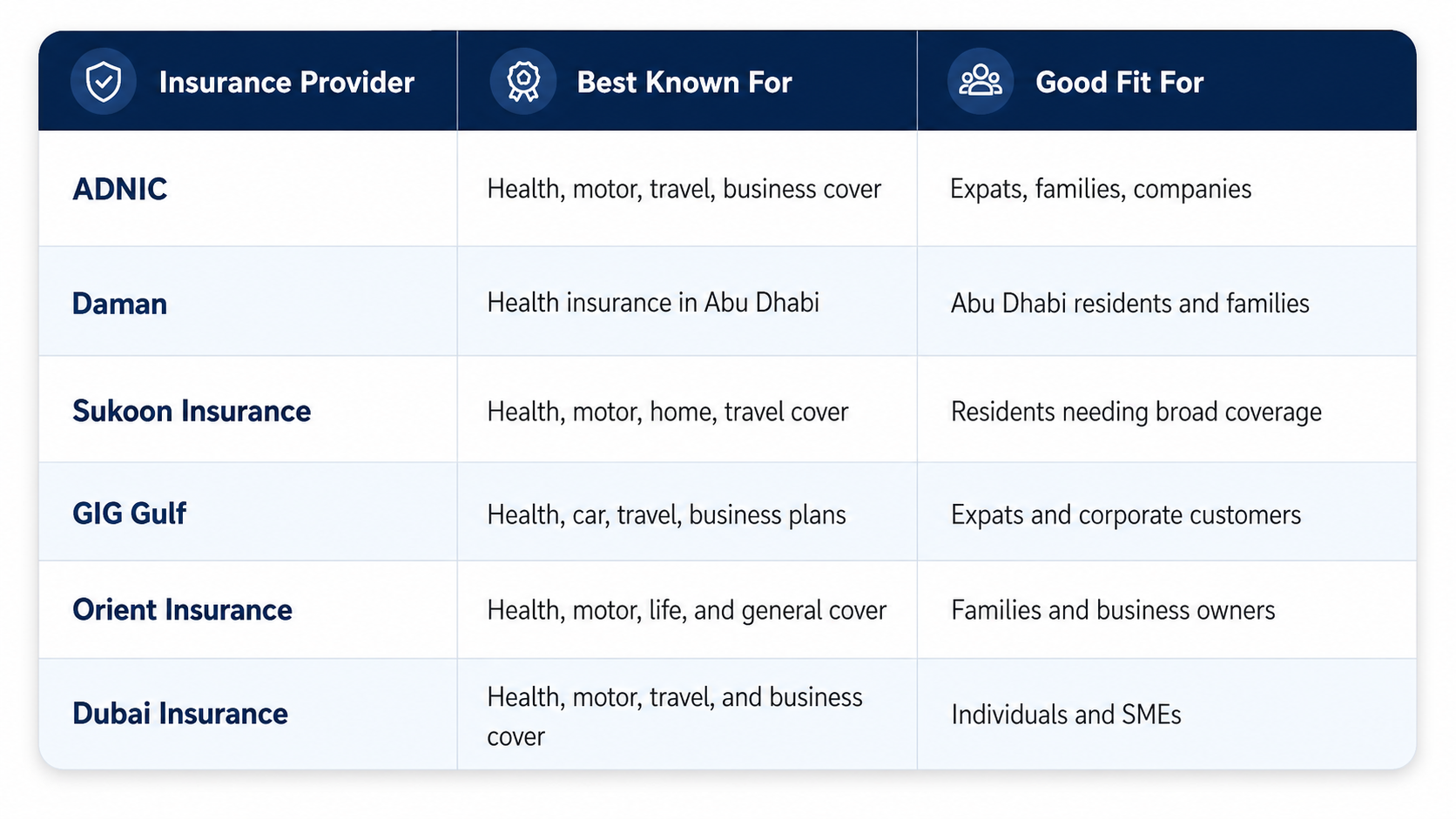

Insurance Provider | Best Known For | Good Fit For |

ADNIC | Health, motor, travel, business cover | Expats, families, companies |

Daman | Health insurance in Abu Dhabi | Abu Dhabi residents and families |

Sukoon Insurance | Health, motor, home, travel cover | Residents needing broad coverage |

GIG Gulf | Health, car, travel, business plans | Expats and corporate customers |

Orient Insurance | Health, motor, life, and general cover | Families and business owners |

Dubai Insurance | Health, motor, travel, and business cover | Individuals and SMEs |

Do not select an insurer only because the name is popular. Compare claim reviews, hospital or garage network, exclusions, renewal price, customer support, and complaint handling before buying.

Factor | Online Insurance Provider | Broker-Assisted Provider |

Best for | Simple policy comparison | More complex coverage needs |

Speed | Usually faster quote process | May take more discussion |

Support | App, portal, or call center | Human guidance and follow-up |

Price view | Easy to compare premiums | Can explain policy trade-offs |

Policy fit | Good for basic needs | Better for family or business needs |

Claim help | Depends on provider quality | A broker may help with claims |

Both options can work. The better choice depends on how simple or complex your insurance needs are. For a basic car policy, an online comparison may be enough. For family health cover, business insurance, or high-value assets, guided advice can prevent expensive mistakes.

Insurance providers do not all work the same way. Two policies may look similar in price, but the actual experience can differ. One may have better hospital access, smoother approvals, faster motor repair handling, stronger digital support, or clearer policy documents. The provider also matters because complaints and disputes usually start after poor communication. Sanadak is the UAE’s independent financial ombudsman unit for unresolved consumer complaints against licensed financial institutions and insurance companies, but consumers are expected to first try to resolve the issue with the company.

That means your first line of support is still the provider. Choose one that is easy to reach before a problem happens.

Start with the insurance type

Decide whether you need health, car, home, travel, life, or business insurance.

Check licensing first

Make sure the insurer or insurance channel is properly licensed in the UAE.

Compare coverage before price

Look at benefits, limits, exclusions, networks, deductibles, and claim steps.

Read recent UAE insurance reviews

Focus on claim handling, support speed, renewal behavior, and complaint patterns.

Ask for the full policy wording

Do not rely only on sales brochures or quote summaries.

Test customer support before buying

Ask two or three specific questions and see how clearly they answer.

Compare the claim process

Choose a provider that explains claims in simple steps.

Choose a provider that is licensed, clear, and reachable. Do not buy a policy only because the premium is low. Check the policy wording, exclusions, network list, claim process, and renewal conditions before payment. A good provider should answer practical questions without forcing you to guess.

Use comparison websites, insurer portals, Google reviews, app reviews, and public complaint information to compare real customer experience. Look for patterns, not one angry review. If many people mention slow claims, poor approvals, weak support, or unclear renewals, treat that as a warning sign.

Use a licensed broker or advisor when your case is not simple. This is useful for family health plans, business insurance, fleet cover, high-value cars, life insurance, and policies with many exclusions. A good advisor should explain the policy in plain English and help you compare real value, not just the premium.

Checkpoint | What to Review | Score 1-5 |

|---|---|---|

Licensing | Registered or licensed in UAE | |

Coverage fit | Matches your real insurance need | |

Claim process | Clear steps and timelines | |

Network access | Hospitals, clinics, garages, partners | |

Exclusions | Easy to understand before buying | |

Customer support | Fast, clear, and reachable | |

Reviews | Strong recent customer feedback | |

Renewal terms | Clear pricing and policy changes | |

Digital access | App, portal, email, documents | |

Complaint handling | Clear internal complaint process |

Use this scorecard before buying. Any provider scoring weak on claims, support, exclusions, or network access should not be your first choice.

Choosing the right insurance provider in the UAE is a practical decision, not a branding decision. Before buying, check:

Licensing and UAE authorization

Coverage limits and exclusions

Claim process and support quality

Hospital, clinic, or garage network

Recent UAE insurance reviews

Renewal terms and extra charges

Your next step is simple: shortlist providers, score them using the checklist above, and choose the one that gives the best mix of coverage, support, claim clarity, and price. The right insurance provider is not the one with the loudest offer. It is the one that clearly explains the policy, supports you during claims, and protects you when the problem is real.

There is no single best company for every resident. The best choice depends on your insurance type, budget, network needs, claim support, and whether the provider is properly licensed.

Buy online if your need is simple and you understand the policy. Use a broker if you need family cover, business insurance, high-value car protection, or help comparing complex terms.

Ask what is covered, what is excluded, which providers are in network, how claims are filed, how long approvals take, and what you pay through deductibles or co-payments.

Check whether the insurer is registered or licensed to operate in the UAE. The UAE government states that the Central Bank registers and licenses insurance companies in the country.

Insurance claim rejection in UAE can happen due to missing proof, exclusions, delays, or wrong filing. Learn the real reasons and fixes for 2026.

Compare Takaful vs insurance in UAE for 2026. Learn the key differences, costs, benefits, and which option fits your health, car, family, or business needs.

Can UAE insurance increase after one claim? Learn why premiums may rise, what residents experience, and how to reduce renewal costs.

Learn the hidden side of UAE health insurance that expats often discover too late, including exclusions and co-pays, claim limits, and hospital network issues.